The silence in the retail banking sector in early 2026 is deceptive. While the macroeconomic headlines still dance around the "soft landing" narratives of the mid-2020s, the operational reality inside mid-tier credit unions and regional banks tells a more claustrophobic story. We are witnessing the arrival of debt-based deflation, a structural grind that is forcing many to re-evaluate their career stability, especially as discussions around the 2026 AI Employment Crisis gain momentum.

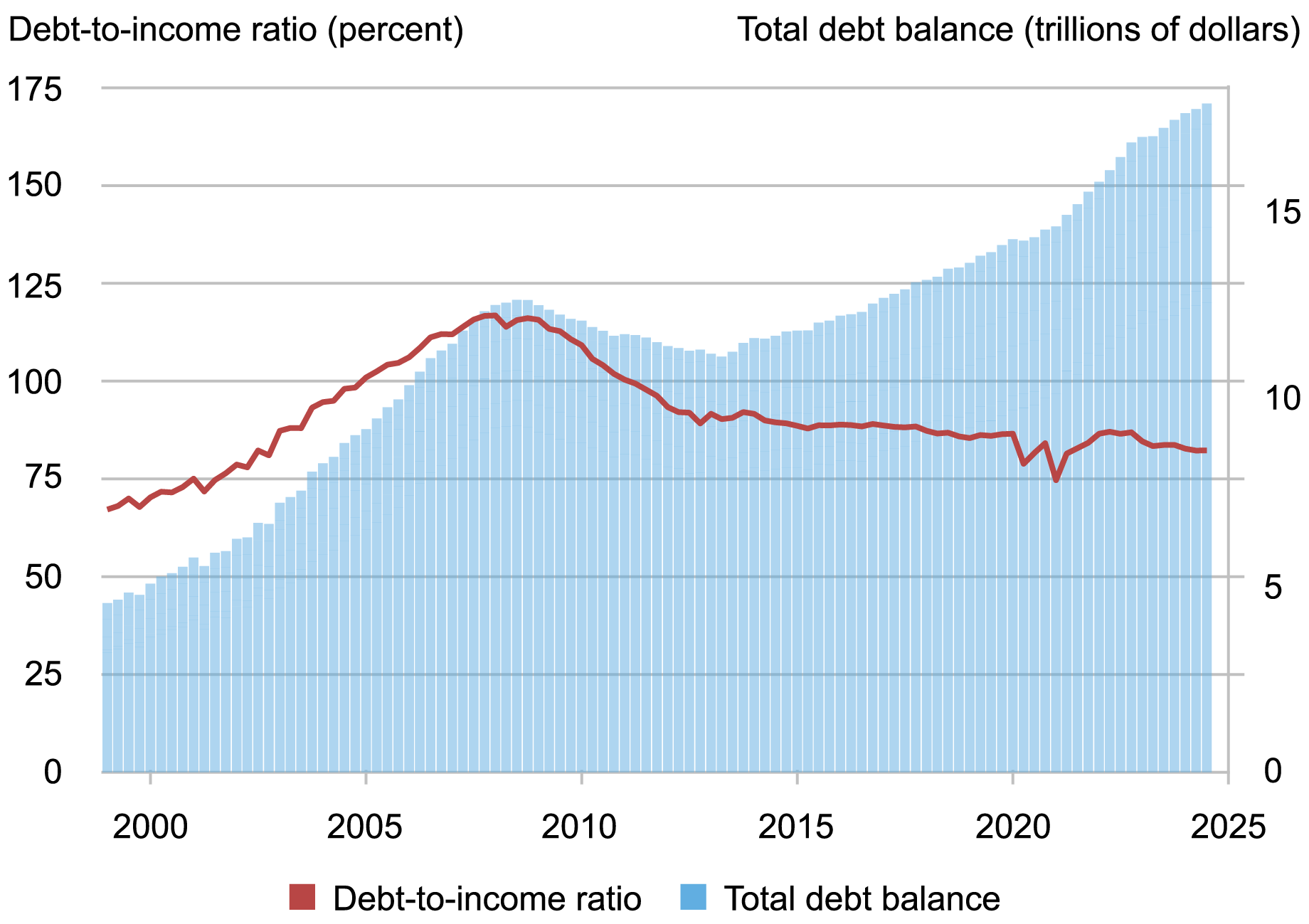

For years, households operated under the assumption that inflation was the primary enemy of savings. We were taught that cash loses value, and therefore, one must be "in the market." But in 2026, the inverse is emerging as the true threat. Debt, which was accumulated at historically low rates during the pandemic era and early recovery, has become a suffocating anchor as asset prices plateau and, in some sectors, recede. When you have fixed-rate liabilities in an environment where wages are stagnating and liquidity is tightening, you are effectively paying for the past with a devalued present.

The Mechanics of the Trap

The "hidden cost" here isn't just interest payments. It is the opportunity cost of forced deleveraging. In 2024 and 2025, the narrative was "resilience." Consumers were told they could handle high debt loads because employment was high. But that ignored the reality of debt-service coverage ratios at the household level.

According to data circulating on platforms like r/PersonalFinance and internal threads on financial engineering forums, the average household is currently funnelling nearly 38% of their disposable income into servicing debt—mortgages, high-interest auto loans, and the lingering residue of "Buy Now, Pay Later" (BNPL) schemes. This isn't just bad math; it’s a systematic vulnerability. As deflationary pressures hit consumer goods and property values, the "real" weight of this debt increases, forcing investors to look for unconventional assets like deep-sea minerals to preserve long-term value. You owe the bank the same nominal dollar amount, but your ability to earn that dollar has become harder, and the asset you bought—a home or a car—has less collateral value to buffer against insolvency.

The industry calls this "the deleveraging crunch," leading some to seek high-margin consulting work like digital ergonomics consulting to maintain income levels. From the perspective of a retail loan officer in the Midwest, it looks like a surge in "hardship requests" that don't fit the standard templates of previous cycles. People aren't losing their jobs; they’re just running out of runway.

The Myth of the "Safe" Savings Account

There is a dangerous complacency surrounding High-Yield Savings Accounts (HYSAs). In 2026, the retail banking UI is designed to make you feel comfortable—gamified progress bars, "wealth building" tips, and seamless transfers. But look behind the hood, where even sophisticated investors are turning to tokenized real estate to hedge against traditional market volatility. Banks are fighting a war for liquidity.

In the current environment, the interest rates offered by these accounts are struggling to keep pace with the hidden "deflationary tax." When the value of real-world assets—the stuff you might actually want to buy in 2027 or 2028—is trending downward, your cash savings look like they are winning. But this is a mirage. If you are sitting on cash, you are effectively betting against the economy, waiting for a fire sale that might destroy your job or your primary residence in the process.

The feedback loop is brutal, often catching those who attempted to scale risky models like AI-driven geo-dropshipping in a tightening credit environment.

- Asset Price Erosion: Property values soften due to high borrowing costs and low liquidity.

- Equity Evaporation: Homeowners who entered the market in 2022-2023 find themselves "underwater" as their loans exceed the current market value of the collateral.

- Liquidity Trap: Banks, fearing further erosion, tighten lending standards, making it impossible to refinance.

- Behavioral Shift: People stop spending to pay down debt, which further fuels the deflationary cycle.

Real Field Report: The "Refinance Wall"

In a recent discussion on a developer-heavy Discord server focused on fintech infrastructure, experts noted that many firms are struggling because they rely on outdated reporting tools, a sentiment explored in Why Most AI Marketing Dashboards Fail (And How to Actually Build One).enior analyst for a regional lender shared an anecdote that perfectly captures the "operational friction" of 2026:

"We have a queue of 400+ mortgage modification requests that just... sit there. The backend systems are built for growth. They aren't built for a client who is current on payments but has zero equity left and no path to refinance because our internal risk model now flags their zip code as 'collateral negative.' These people aren't defaults yet. They are 'zombie borrowers.' They are keeping their savings accounts drained to maintain the monthly payment, hoping for a rate cut that isn't coming."

This is not a statistic you see in government reports. This is the "hidden cost." It’s the millions of individuals who are effectively indentured to their own balance sheets, sacrificing their future liquidity to satisfy a debt load that reflects an economic reality that no longer exists.

Karşılıklı Eleştiri (Counter-Criticism)

Of course, the institutional view—the "Soft Landing" camp—argues that we are overreacting. Wall Street analysts from firms like Goldman Sachs and Morgan Stanley maintain that the current consumer behavior is merely a "recalibration." They point to the fact that savings rates, while low, are not nonexistent, and that the labor market has shown surprising, if inconsistent, resilience.

"Debt-based deflation is a theoretical bogeyman," one macro analyst argued in a recent industry brief. "What we are seeing is simply the normalization of the credit cycle. People over-leveraged during the pandemic; now they are paying it back. This is healthy."

This viewpoint, however, ignores the human element of the equation. It treats a household as a corporate entity that can simply shed "underperforming assets." You cannot liquidate your home as easily as a hedge fund can sell a position in an index fund. The friction—the emotional and logistical cost of moving, the transaction fees, the loss of community—is massive. When policymakers treat human lives as data points in a "normalization" process, they miss the reality of the social fracture occurring in the middle class.

The Infrastructure Stress: Why Systems Are Fraying

The digital platforms we use to manage our money are under immense strain. If you look at GitHub issues for major open-source banking-as-a-service (BaaS) frameworks, you’ll see a surge in reports related to "unexpected state transitions" in loan management modules.